Sparkle, by former Diamond bank CEO Uzoma Dozie, finally goes live. Here is all you need to know.

The former Diamond Bank CEO Uzoma Dozie has announced the official launch of his new digital bank, Sparkle. This announcement comes 11 months after he mooted the idea in August 2019. How does Sparkle stand against the likes of Kuda, Rubies and ALAT by Wema?

Sparkle has officially launched, 11 months after first public mention.

The former Diamond Bank CEO, Uzoma Dozie has announced the official launch of Sparkle, a new digital bank. This official launch comes 11 months after Uzoma mooted the idea in August 2019.

Following the successful merger of Diamond Bank and Access Bank in March 2019, Uzoma announced five months later that “Sparkle is now being developed to allow people to do more whilst allowing businesses to be more.” It is a new iteration of what it means to support retailers, businesses and individuals in Nigeria, Uzoma said at the time.

🗞️NEWS: Former Diamond Bank Group MD has announced his next mission.

— Benjamindada.com, tech blog (@dadabenblog) August 1, 2019

Uzoma Dozie announces new company that will provide financial & lifestyle services to Nigeria's multi-million dollar retail sector

Thread 👇🏾 pic.twitter.com/Y2iUgFPUPl

Since August 2019, Sparkle has received a microfinance banking license from the Central Bank of Nigeria (like most of the existing digital banks). It has joined Women’s World Banking, a non-profit working to ensure greater financial inclusion for women, their families and communities in emerging markets. Uzoma was previously a board member of the organisation.

Sparkle has also joined Open Banking Nigeria, a non-profit organisation of stakeholders in banking, fintech and risk management working together to transform and advocate open banking in Nigeria and Africa, by extension.

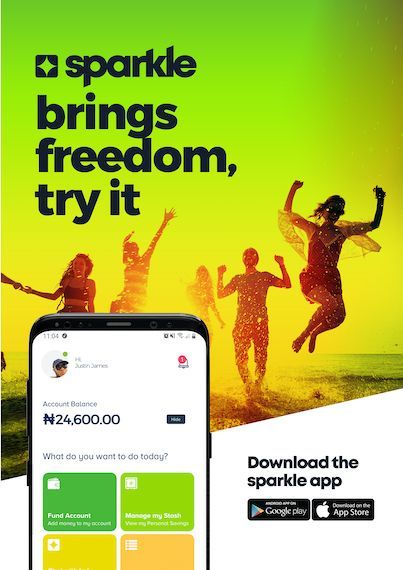

Today, Sparkle is officially launching its mobile app—available on iOS and Android—to give customers full and free access to one account that offers multiple services and different wallets. As of press time, Sparkle features such as "Buy Airtime", "Pay Bills", "QR Payment", "Business Account", and virtual and physical debit cards are still "coming soon" (more on these features later).

The Sparkle Business Account is particularly interesting to watch out for. It plans to offer small and medium enterprises (SMEs) an easy way to manage their accounting, including payroll and expenses, as well as provide business support solutions such as taxation, inventory management, invoicing and payment scheduling.

Sparkle said it is partnering with Visa, Microsoft and PwC Nigeria to achieve its vision of redefining Nigerian commerce. With this partnership, Sparkle will have access to leading expertise in APIs, cloud computing, data science, machine learning, tax and financial advisory services to provide best value for its customers.

"Sparkle will be transformational for Nigerians across the globe," –Uzoma Dozie, who has taken on the title of Chief Sparkler, said. "And I am hugely excited to be launching it today."

Sparkle is redefining Nigerian commerce by merging financial services with a seamless lifestyle solution. We are removing barriers using technology and data, and driving inclusion at scale. In doing so, we are empowering Nigerians to fulfill their potential, democratizing access to valuable solutions for both business and personal needs.

Is Sparkle different from other fintechs or Digital Banks?

There is a plethora of apps in the finance category on Google’s Play Store and Apple’s App Store. These apps range from bank apps used for digital and mobile banking to fintech apps which has little or no differentiating features among them—that is the league Sparkle will be playing in.

On Sparkle, users will be able to see their daily, weekly and monthly spending patterns with detailed breakdown by category. This feature is the whole gamut of Reach, an expense tracking and budgeting app which also allow users to take loan and invest. But it is good Sparkle has such in-app feature, in addition to the typical account statements banks and some fintechs provide.

Also, there are features such as Sparkle Stash, which allow users to save towards specific goals; Indy, a 24/7 financial buddy and customer support chatbot; and SparklePay, which allows users to send money with a link, even to people whose account numbers they don't have.

Again, SparklePay is essentially reverse-engineered PiggyLink, a feature on Piggyvest that allows users to receive payment from anyone. And Sparkle Stash is the mainstay of savings apps. Cowrywise even has a feature called ‘Stash’. Like Cowrywise’s Stash, Sparkle Stash does not offer interests. In fact, Sparkle says "we don’t offer any interests on our savings, but we plan to [do so] in the nearest future. A mouth-watering interest rate for all that wait."

Sparkle is a digital bank and it will be good to see how it stands against ALAT by Wema Bank—Nigeria’s first fully digital bank, Rubies, Kuda, and Eyowo—a mobile money-digital bank by Softcom. But as stated earlier, most of its features, including Buy Airtime, Pay Bills, QR Payment, Sparkle Card and Business Account are "coming soon". Hence, the odds are currently stacked against it in comparison to other digital banks.

Sparkle is offering its first 200,000 users 1-year free banking till June 2021.

Meanwhile, Sparkle says it is offering its first 200,000 users one-year free banking till June 2021 after which there will be charges for transfers to other banks. This is unlike Kuda Bank’s too-good-to-be-true offer of 25 free bank transfers every month for life. Since its release in February 2020, Sparkle has recorded 1,000+ downloads in the Play Store alone.

In conclusion, Uzoma Dozie asks Nigerians to join Sparkle in making "history as we enter the future of commerce and look towards this exciting phase of growth". He said, "We are working with global partners to unleash freedom, flexibility and transparency in Nigeria. We are helping to drive forward the growth of Nigeria’s budding entrepreneurs and individuals".

Comments ()