BD Insider, Letter 67 on CBN crypto ban, Providus, Rubies, Disha and more...

A deep dive into CBN's crypto ban, Providus bank virtual account services withdrawal, Rubies Issue with NIBSS, Disha's proposed shutdown and more.

Editor's note: Today, for the first time, we are making our newsletter into a public post for everyone to enjoy. Our newsletter subscribers get this news first and can take action before everyone else sees the news.

Hi BD Insider,

Benjamin (and 'Hachi) here with some commentary on all the CBN <> financial services drama that took place, amidst other tech and startup news of the previous week.

Before I delve right in, I'd like to say a big thank you to everyone who has stuck with us from our very first newsletter up until this time. It's been an honour to serve you. If you have received more than 50 newsletters from us, please let me know and I'd personally reach out to you.

So, as you know, last week was intense. And if you work in Nigeria's Fintech (particularly, crypto) industry, you can testify.

This newsletter will cover:

- CBN vs the Financial Services Industry (FSI)

- Ban on Crypto facilitation

- Rubies microfinance bank issue with the Central Switch

- Providus Withdrawal of Virtual Account Services

- Why Virtual accounts are necessary

- DishaNG shutdown

- And more...

₿ CBN vs FSI in Nigeria

#CBN prohibits regulated institutions from dealing in cryptocurrencies or facilitating payments for cryptocurrency exchanges...https://t.co/OQ6MvQB8O1

— Central Bank of Nigeria (@cenbank) February 5, 2021

Part 1: The Ban on Crypto Facilitation

The Financial Services Industry is a very regulated space. Particularly so in Nigeria, where there is an Apex Bank, the Central Bank of Nigeria (CBN).

Current and intending players in this space are well aware of the challenges. And in fact, have had to deal with stringent regulation when it comes to getting a Licence to float their practice.

In November 2018, Benjamindada.com published an explainer on the confusing "₦5 billion" requirement for specific financial services licence. Since then, things had been relatively stable, featuring a few circulars here and there but nothing as drastic as what we saw last week.

February 5, 2021, the entire country was thrown into shock when the CBN, led by Governor Godwin Emefiele, released a notice asking all regulated financial bodies to desist from trading in cryptocurrencies or facilitating crypto trade.

The content of the notice was not new. The CBN had previously warned regulated financial bodies of their association with crypto.

However, this time was different. The tone was menacing, and sanctions were threatened.

What followed was one of the most chaotic nights in the history of Nigerian Tech. And brought back bad memories of the regulatory slam that brought a hold to bike-hailing companies (in Lagos).

As an effect of the announcement, naira funding for all Nigerian crypto companies has been halted. While companies were initially allowing withdrawals, some like Quidax have now put an embargo on that too.

Although insider information is that the companies have formed a small lobby group to talk to the regulators, there is still some level of unrest.

If lobbying fails, the immediate alternative will be to pivot to P2P platforms where users can trade among themselves with the startups providing escrow services.

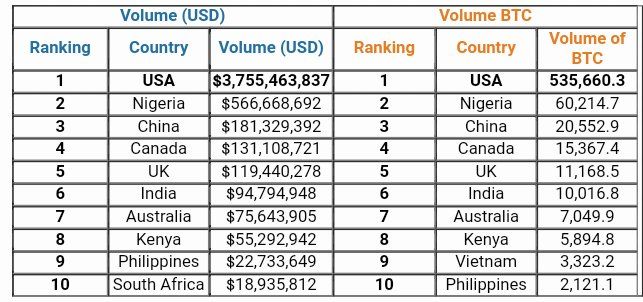

Nigeria already ranked second on Paxful, one of the world's biggest P2P crypto trading platforms in 2020. Regardless of whether CBN's decision is reversed or not, you can expect the numbers behind P2P transactions to skyrocket in the coming months.

Part 2: Rubies Microfinance Bank Issue

#Rubiesbank pic.twitter.com/7hmleYLQ0d

— Rubies MFB (@rubies_ng) February 3, 2021

Not much is known about the reason for "Rubies issue" with the Central Switch which is NIBSS (Nigeria Inter-Bank Settlement System Plc).

As the Central Switch, they facilitate many services that allow banks and OFIs to talk to each other. For instance, instant transfer from one bank to another bank (via NIP—NIBSS Instant Payment). Also, they act as the PTSA (Payment Terminal Service Aggregator) for payments in the country. Terminals include PoS and ATM. NIBSS was incorporated 27 years ago and is owned by all licensed banks including CBN, the regulator.

In short, you know you have arrived as a business in Nigeria's FSI space when you are listed on NIP. To be listed, there are some regulatory hurdles to cross. For instance, you must be approved by CBN (can be either a commercial bank, microfinance bank [MfB] or MMO)

Rubies is a fintech platform with an MfB license and as such are listed on NIP.

However, on Wednesday, February 3, 2021, they confirmed that they were having an issue with the Central Switch. "We are currently experiencing a network downtime with the central switch as such transfers are failing", says Rubies.

There are speculations that this downtime that is specific to Rubies is a form of sanction from the CBN. Now, the reason for the sanction has been kept away from the public, thus far.

Industry players say it might have been as a result of them enabling transactions outside their scope, for either an International Money Transfer Operator (IMTO) or a Crypto company.

Whatever the case may be, a key takeaway is that this transfer downtime is not industry-wide, which then brings me to the issue with Providus Bank.

Part 3: Providus Withdrawal of Virtual Account Services

We wish to announce that our virtual payment services are currently unavailable. In the meantime, customers are advised to use alternative payment options. Thank you.

— ProvidusBank (@ProvidusBank) February 7, 2021

Two days after the crypto announcement, fintech users on various services started to notice that they could no longer fund their wallets via bank transfers to an account.

"Pay with Bank Transfer" is a relatively new payment (/ funding) method made mainstream by Monnify, a product of TeamApt that is run in partnership with a Bank.

"We received official communication from our partner bank - Providus Bank that they would no longer be supporting the virtual accounts service with immediate effect", reads an official statement by the Monnify Team. Indeed, on Sunday, February 7, 2021, Providus Bank told the public through a tweet, that their "virtual payment services are currently unavailable".

Monnify, which is arguably the leading provider of such virtual account services had mentioned in their statement that they will be back with a new partner bank by today, Wednesday.

This service withdrawal affected startups that used the Monnify service in serving their customers. The affected startups include: Piggyvest, Risevest, Abeg, Kolopay, Trove, and Cowrywise. We have questions:

- What is next for startups that have come to rely on this service?

- How did "Pay with Bank Transfer" rise to such prominence?

- Is this an industry-wide sanction or just a Providus decision?Here are the answers, respectively:

- Startups, like Monnify itself, will have to find alternative providers. Already, startups like Piggyvest and Risevest have already switched to Wema Bank (virtual) accounts provided by Flutterwave

- This will be answered in the following section

- Since substitute services like that of FLW<>Wema is running, one can assume it's just a Providus Management decisionMy question is for how long will they run? If not, when will Providus' service be back up?

🍪 Bonus: How did Nigerians and startups come to rely on virtual accounts

BD Insider, grab some 🍿and let me take you on a journey.

Over the past 20 years, payments in Nigeria evolved tremendously.

Ten years ago, NIBSS introduced an account-number based, online-real-time Inter-Bank payment solution called NIBSS Instant Payment (NIP). It was a huge improvement from NIBSS Electronic Funds Transfer (NEFT) that went through a clearing process and took 24 hours (next day) before the recipient gets value (money). Over the years, the majority of Nigerians proved that they loved NIP over NEFT. NIP grew by 303% in just four years, between 2014 and 2018 while NEFT was declining. In 2018, NIP processed ₦80.4 trillion while NEFT processed just ₦11.6 trillion.

As recent as five years ago, if you wanted to pay online in Nigeria, you were limited to "Pay with Card".

Interswitch's web pay and/or payment gateway was the de facto gateway for payment. Flutterwave (2014) and Paystack (2015) were just settling into the payment space. And building wrappers around Interswitch's infrastructure.

Now, the drawback of "Pay with Card" is that there are only a few banked Nigerians that use payment cards. Thus, we have more people with bank accounts than with cards tied to them. So, "Pay with Card" was excluding banked customers from paying online. Left to me and many other Nigerians (who do not want to enter their card details anywhere), we are okay to pay via bank transfers. But it simply wasn't possible to pay with bank transfer online. Already, paying with a transfer offline was and is hectic because "the person with the phone (to get transaction alert) is not on seat".

Anyway, fast forward to June 2017 and Paystack launched their "Pay with Bank" feature.

"Pay with Bank" finally allowed customers to pay by entering just their account number and authorising the payment gateway to do a direct debit on their account. Boom! That was big. However, it came with some drawbacks that made "Pay with Bank Transfers" imminent. They include: Reach, Push vs Pull, and User behaviour

- Reach: "Pay with Bank" is limited to the banks that payment gateways have direct integrations to. So, for instance, when Paystack first started only about 8 banks were on their list for "Pay with Bank". So, only customers with those listed banks could pay online (via Paystack). Meanwhile, NIP has all the 23 Deposit Money Banks (DMBs) plus MfBs, and licensed MMOs.

- Pull vs Push: "Pay with Bank" runs on direct debit by the payment processor, while "Pay with Bank transfer" is initiated by the customer (which is more natural to the user).

- User behaviour: Because many people are already used to transferring money to an account as a form of payment. "Pay with Bank transfers" benefitted greatly from that already existing user behaviour. And as such, adoption has been rapid and high.So, it was the opening up of virtual accounts for customers to make payments that led to the "Pay with Bank transfers" functionality we have all come to love.

🚪 DishaNG announces shutdown but maybe not

Disha.ng is an online no-code tool for creators to showcase themselves and their work through a one-page site.

It was founded in 2019 by executives of Cregital; Evans Akanno and Rufus Oyemade, alongside Blessing Abeng, who came in as the Chief Marketing Officer in February 2020.

The company experienced huge traction with massive fan (user) love within their one-year-plus of operation. According to a statement on their home page, they "achieved 100% growth monthly...and over 20K users globally".

Yet, on Saturday, February 6, 2021, they announced that they will be completing shutting down their service on December 31, 2022.

Disha's statement did not give a reason for their decision, other than, "shortfalls with the platform’s vision" and other unresolved misalignments. Prior to the corporate announcement, Mrs Abeng tweeted about her exit from the startup because "Disha evolved its dream and trajectory in a way that no longer aligned with the vision I committed to". Her final day was the "last day of August (2020)".

Thanks to our community for sharing their thoughts and wishes on keeping Disha online after our shutdown notice. We are currently considering new options for our company and will share an update as soon as we have made a resolution.

— Disha (@getdisha) February 9, 2021

Although the company's statement indicated that they had considered and exhausted every option available to them, recent communication indicates otherwise. "We are currently considering new options for our company and will share an update as soon as we have made a resolution", says a tweet from the company.

💸 Fundraising

Here are some of the recent startup fundraises across Africa that you should be aware of:

- Ghanian Agritech company, Agrocenta has raised $790k in a pre-series A round. The raise will be used to develop the agritech’s existing smallholder farmer inclusion programs.

- South African startup Aerobotics raises $17M to scale its AI-for-agriculture platform

- Kenya's Gro Intelligence, an AI-powered insights company, raised $85-million in Series B fundingTip: If you're looking to improve your take-home (salary) by moving jobs, companies that have just raised are a great place to apply. Companies almost always hire after a significant raise.

📰 Things we found interesting

Here are some of the most exciting stories we've written and read over the last seven days:

- We wrote a detailed explainer on how the CBN's actions affect crypto users and the startup community.

- Risevest wants to bring the best investment opportunities to Africans Read just how they plan on doing so.

- Salescabal has relaunched as Bumpa - an e-commerce solution for businesses.

- An uber, a Christian woman, and Jesus Christ walk into a bar. Read marketing lessons from a social media debacle that consumed Twitter a few weeks ago.

- How to be a genius. Lessons from the lives of geniuses.

- Doktorconnect launches to give people cheap and affordable access to doctors.

- Chrome pulled one of the most popular extensions from its store, Read why.

🚪 Jobs and Opportunities

In addition to last week's list of jobs, events, and other opportunities, check these out, too:

- BuyCoins is hiring a Senior Product Designer

- Piggyvest is hiring Customer Success Interns

- BuyCoins is hiring a Customer Success Associate

- No-code professionals can apply for jobs here

🙏 Thanks for reading

Hope this newsletter was helpful. Reach me directly by replying this email.

Regards,

Benjamin

Subscribe below.