What's up with virtual dollar cards in Nigeria? And what's the alternative

"Life-saving" virtual dollar cards in Nigeria has come under attack, as leading provider pulls plug. What could make them pull the plug and what are the alternatives for consumers and fintechs alike?

Barter, popularly known for its virtual dollar card service, announced on Friday, July 15, 2022, that it was shutting down its virtual card service.

Barter by Flutterwave was the first of many Nigerian fintechs to break the hearts of fintech-savvy Nigerians with the withdrawal of their virtual card service. According to an email Barter sent to users, "effective Sunday, 17th July 2022, all our Virtual Dollar cards will be unavailable for any transactions and purchases." It attributes this unavailability to "an update from our card partner, which will cause the card service to be unavailable for an extended period of time."

When I saw the Barter announcement, my first question was "Who is this card partner?" This is because, one would expect an African payment giant like Flutterwave to be speaking directly to the card schemes, as opposed to working through a card-issuing company to issue Mastercard.

Flutterwave used to issue Visa cards until they switched to Mastercard. Startups who had previously issued virtual Visa dollar cards provided by Barter tell me that it wasn't reliable enough. Hence, why they switched to Union54. Even Flutterwave now "partners" (AKA use) with Union54 (for Barter).

Who is Union54?

Union54 is the Zambian startup making it seamless, reliable, and rewarding to issue virtual dollar cards in Africa.

Union54 was officially founded in 2021 by an entrepreneurial couple, Perseus Mlambo and Alessandra Martini. Perseus and his wife have been building digital financial services since 2015 when they launched Zazu Africa. Zazu is a neobank and thus, needed to issue debit cards to allow its users to spend their money anywhere. But it just wasn't working, owing to sponsor bank delays in issuing those cards—"at one point they had to wait for 18 months", Perseus told Tage of TechCrunch.

As a fix, they decided to go direct to Mastercard. They succeeded and became a Mastercard Principle member—allowing them to issue and acquire card transactions. Their decision at Zazu to make this issuing capability available to other African fintechs is what birthed Union54.

The work Perseus and Alessandra are doing is so crucial to the African continent, especially Nigeria where there are restrictions on international commerce. But also in Zambia, their home country, where only about 10% of the adult population has a debit card. Hence, financially excluded from participating in the global economy.

Little wonder, that in less than a year, Union54 raised a $15.1 million Seed from investors all over the world including Tiger Global and Nigerian neobank founder, Babs Ogundeyi of Kuda Bank. They are also the first Zambian startup to get into Y Combinator, the leading global accelerator.

With Union54's APIs, fintechs are able to issue debit cards without worrying about all the complexities of the card business. Union54 takes care of the required Bank sponsorship needed to work with the selected Card scheme (Mastercard, in this case). They also facilitate transaction processing and settlement.

As of October 2021, Union54 said more than 50 companies are currently in its API sandbox environment. Four of them—Flutterwave, PayDay, Plumter, and Bitmama— were live. Union54's clientele includes existing startups and new startups "founded on the basis of Union54’s availability", Perseus boasts without mincing words. He is not wrong. Startups that offer one debit card for all your bank accounts would fall neatly into this bucket that Perseus describes as being founded on Union54's availability.

Similarly, we project that Union54's clientele would have more than quadrupled in the last six months. This growth we believe to be driven by organic marketing—earned media and word of mouth referral—due to the novelty of its solution, timing, the prevailing consumer need, and additional revenue line. On revenue, Union54 is the "only company in Africa that would give you [fintechs] the interchange.” Interchange fees typically accrue to issuers and processors, which would be Union54, in this case. But TechCrunch reports that customers of Union54 (the fintechs that on-issue cards through them) earn 1% on each card transaction carried out by the cardholder.

Union54 has also invested in a couple of African infrastructural and cross-border payment startups we know.

The current virtual dollar card outage reported by tens of fintechs in Nigeria is believed to be due to Union54's downtime.

Union54's message to its Partners on its virtual cards' downtime

Dear Partners;

Despite our best efforts, on 18th July, cards will stop working. We have a number of upgrades and work streams we will be implementing which might take us ~ 6 weeks before we can resume service again.

As a reminder, you can defund cards and process float funds via: https://docs.union54.technology/docs/float-refunds. Please make sure to defund all cards by 17th July 2022 in order for us to effect a bank transfer of any remaining floating float funds on the 20th July.

We had hoped to avoid this hiatus but it had proved impossible to do so. As such, please accept our apologies for the impact on your business and know that we will back with a stronger and more resilient product.

For the purpose of clarity: new card issuance and transaction processing will stop on the 18th July. All issued cards will not work during this hiatus.

Onwards and upwards.

So, why exactly is Union54 down, and for how long?

No one knows the exact cause of the downtime—not even the founders of startups using Union54. I'm in three founder-focused groups, and I've chatted directly to some of the founders of startups that have publicly come out to announce their virtual dollar card downtime.

Regarding how long Union54's card-issuing offering would be down, I estimate six to ten weeks. One affected founder told me, "we'd be back up in six weeks" via private message. Another founder said "Probably 7 ish weeks". So, I've added an additional three weeks to account for any uncertainties.

A recurring theme I have heard from speaking with founders is that Union54 is trying to resolve some issues with Mastercard. But that the founders don't know the details of those issues.

What could these issues be? And could it be similar to some of the issues that Flutterwave might have faced some years back with Visa?

A major issue many acquiring players in the Card value chain face is a high rate of chargebacks and fraud. A chargeback is a dispute raised by a customer when they didn't get value for a transaction. Fraud occurs when someone tries to use a Card that they are not authorised to use to authenticate a transaction. The fraudulent use of a chargeback is when customers try to secure refunds even when they got value. So, they reach out to the issuer/bank to initiate the chargeback process.

With chargeback processing, there are strict resolution timelines otherwise the customer will get their value back, "System accept". Card schemes have a low tolerance for high volumes of chargebacks filed through an acquirer. Thus, many acquirers are willing to turn off merchants on their platform till they can get their processes in order.

Regarding Union54, it's possible that end users of their issued cards are using it to perpetrate fraud on other payment gateways and that's raising a recurring flag with their card scheme, Mastercard. So, Union54 might be taking a step back to build better chargeback, reconciliation, and settlement processes.

On the other hand, the commercialisation of the card-issuing offering from Union54 might not suffice for their relationship with Mastercard. So, two things to note here. Before now, Mastercard didn't offer any direct licence to digital-first players, partly cause those players couldn't afford Mastercard's quarterly fees (which are in dollars). Banks, act as both BIN sponsors and settlement partners to facilitate card issuing and transaction settlement, respectively. But Union54's offering makes them a non-bank issuer with the expected backing of a Bank.

Operating in the card space is hard, and more than ever, consumers are demanding ways to spend their money globally. In the meantime, customers can do three things:

- request foreign domiciliary accounts from their local banks.

- continue to seek alternative consumer fintechs offering virtual dollar cards. For example, Sudo Africa, Chipper Cash, Mono, and Changera virtual dollars card offerings. More examples are contained in the link above.

- seek alternatives that allow above the $20 international spending limit on naira cards. I don't know why, but gomoney reviewed my naira card spending limit to $100. So, maybe try them.

Consumer fintechs like—Barter, Eversend, GetEquity, PayDay, Vesti, Busha—who have publicly announced the shut down of their virtual dollar card service will now look to other providers for this solution. Doesn't seem like there is any readily available. Perhaps, we are all doomed to check back in two months.

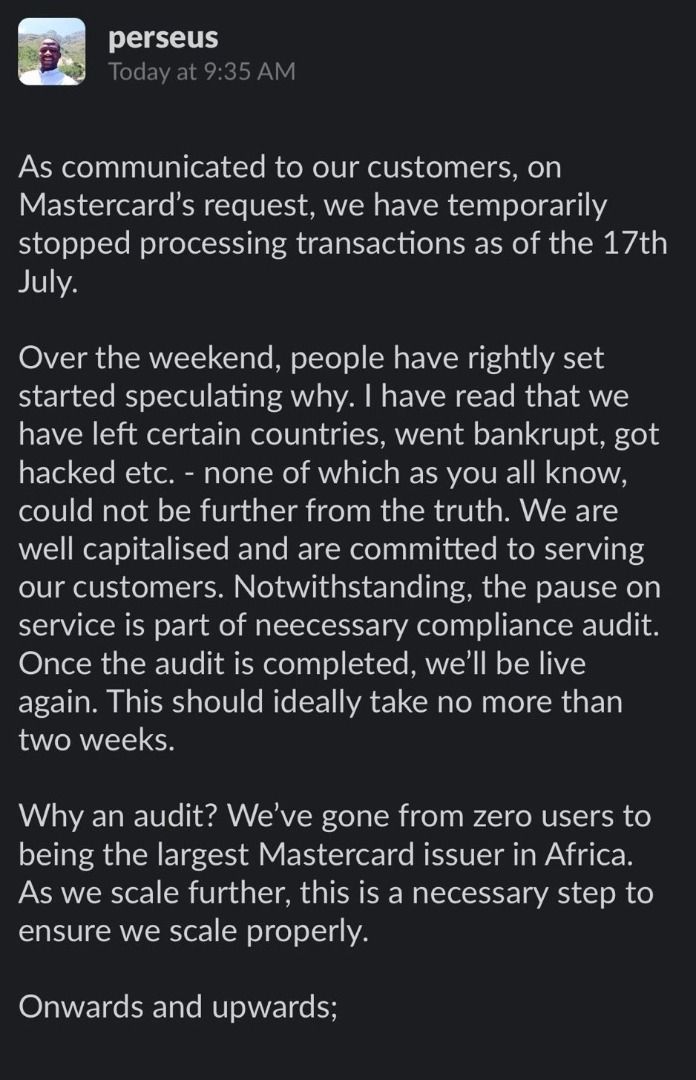

Union54 is pausing for a "necessary compliance audit"

On Monday (July 18, 2o22), Union54's CEO Perseus Mlambo tweeted a screenshot of an internal Slack message, stating that "the pause on service is part of a necessary compliance audit" which will take place within two weeks.

Editor's Note:

- This is a developing story.

- Changera virtual dollar card is now available. We have made this update ( July 17, 2022).

- We've added a full transcript of the message from Union54 to its partners (July 18, 2022).

- We added examples of other virtual dollar card providers (July 18, 2022)

- We added an update from Union54's CEO comment regarding the issue. (July 18, 2022)

Comments ()