Why would PiggyBank introduce a Flex

On Monday, June 25, Piggybank.ng, an impressive Nigerian fintech startup focused on savings released new updates to their service. The updates included; introduction of PiggyFlex, higher interest rates, and PiggyPoints conversion to cash.

On Monday, June 25, Piggybank.ng, an impressive Nigerian fintech startup focused on savings released new updates to their service. The updates included; introduction of PiggyFlex, higher interest rates, and PiggyPoints conversion to cash.

N.B - if this is your first time hearing about PiggyBank, please read this first.

Let's talk about our new update, shall we?

— PiggyBankNG (@PiggyBankNG) June 26, 2018

Of all the updates, I find the Piggy Flex and Points bit to be the most interesting.

On the higher interest rates, a user with a high disposable income (NGN 75,000 - NGN 178,500) seeking the best Return-on-Investment (RoI) is probably better off investing in an agritech platform like ThriveAgric. There the rates are sometimes as high as 22% in 10 months compared to PiggyBank's 12-month 12.4% on Safelock, their highest earning savings product.

Piggy Flex

PiggyFlex is a PiggyBank feature where users can withdraw their funds at any time with NO withdrawal fee.

Can there really be a PiggyBank with no withdrawal fee? What happened to "imbibing discipline in users to enable them to save"?

Being a concerned user, I reached out to one of the co-founders seeking clarification. The conversation went thus:

Benjamin Dada: "Why would PiggybankNG, at this time, launch a product that allowed people take their money out at any time, Piggy Flex? What informed that decision?"

Piggybank Co-founder: "PiggyFlex doesn't affect the core of Piggybank. If anything, it makes the entire product extendable and creates room for scale."

While I was trying to come to terms with that, he adds, "PiggyFlex is derived. You can only get money into it when you have money saved in your piggybank...".

"Ah, bingo!", I thought to myself. You need to have money in your PiggyBank savings account before you can move money to your PiggyFlex account.

He concludes by saying "There is a product roadmap and PiggyFlex is an important feature in the grand scheme of things".

In my opinion, PiggyFlex comes with just one unique selling point that is enabling peer-to-peer (P2P) transfers.

Update, Apr. 28, 2019: PiggyFlex has more than just one USP. It could also serves as an embedded expense account for the company to bill users for services supported, like delivery of bank statements.

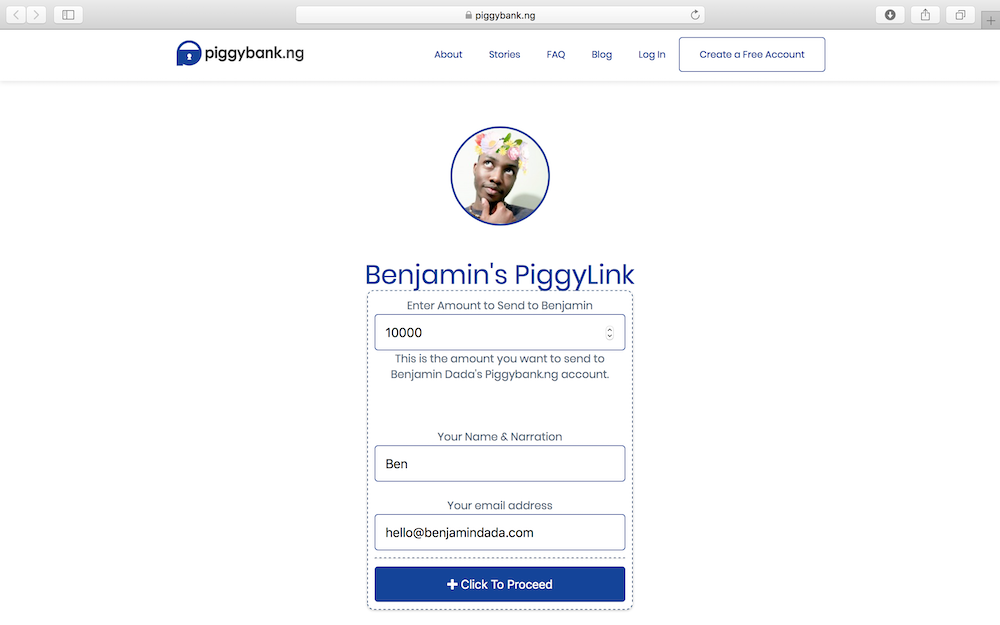

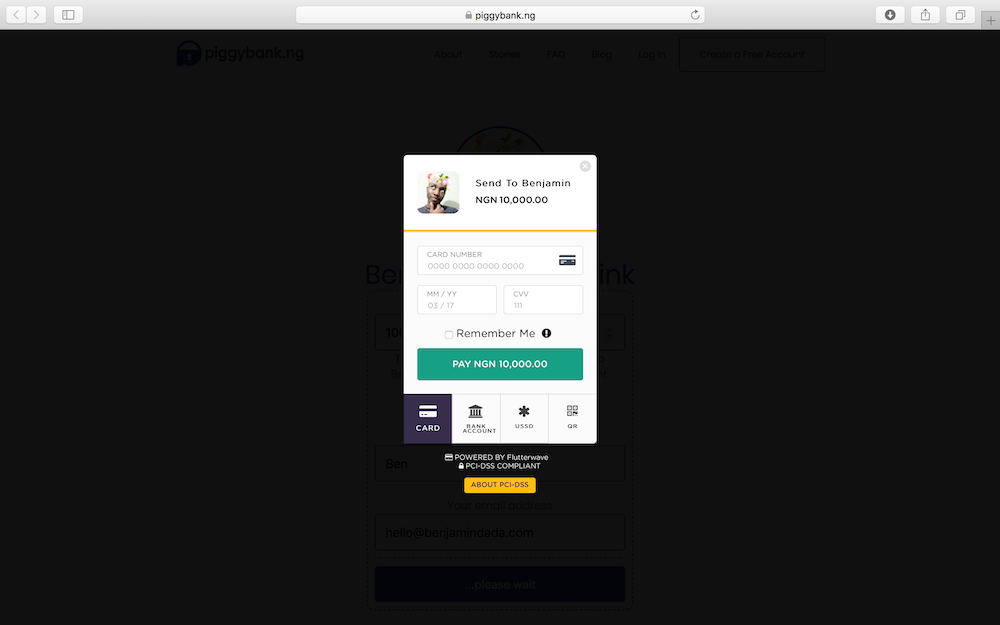

Recall that before PiggyBank came up with the idea of a PiggyFlex sub-account, they had previously introduced PiggyLink, an avenue for their users to get paid by anyone, whether or not they have a PiggyBank account.

The way it works, when a user has created a PiggyLink from the settings section in their dashboard, they can then send it out to the public who then transfers money to them via a card interface.

While this strategy helped in getting funds into the PiggyBank Wallet, users were getting weary of having to leave the platform to send money to another person on the same platform, PiggyBank. So, for one, PiggyFlex helps to solve the problem of P2P transfers on Piggybank.

The other thing that could seem like a selling point is what banks currently offer via a savings account which allows you any time access to your funds (plus some "unnoticeable" interest). So, no, I as a user might as well just move my money back into my bank savings account, except I'm considering re-saving.

In conclusion, PiggyBank's introduction of a PiggyFlex sub-account could see the fintech do more sideways transaction and eventually become an ecosystem for the proliferation of other financial services like P2P lending.

Bonus: PiggyBank might be looking to launch a bot, LOL. It's only right PiggyBank launches a bot, after such a bio.

Learn about the other updates here from PiggyBank themselves.

Update, Apr. 28, 2019: Made structural updates

Comments ()