Inside Getwallets’ pivot to Orchestrate, a payments infrastructure company

Orchestrate (formerly Getwallets) is a payment infrastructure company that give fintechs and merchants access to multiple payment providers with a single integration. But before Orchestrate, there was Getwallets. What changed and what is next?

Fintech in Africa has come a long way since 2015. The ecosystem has grown from a few card-processing payment startups to digital banks, savings & investment platforms, and now, open banking, BaaS & fintech infrastructure startups.

The problems (hence, opportunities) on our continent are enormous because they affect a large number of young people. Thus, solving African challenges does two things: leads to societal impact, and guarantees wealth for the builders, both now and in the future. However, because there is no one way to the solution, we have many “agents of change”, startups springing up to have a go at parts of the problem. To move fast, these startups build in silos, which has now led to solution fragmentation, and limited interoperability, locally and cross-border. Unfortunately, the cross-border differences buoyed by policy, provider coverage, and consumer preferences haven’t helped to unify our development efforts.

Take, for instance, payments in Africa. Each country has a different set of payment methods and payment providers. Narrowing down to East Africa, we know that the M-Pesa payment method is king. But did you know that the M-Pesa offering provided by Safaricom in Kenya was different from the one by Vodacom in Tanzania? Thus a business expanding out of their local country in East Africa still has to integrate multiple providers to ensure coverage in the expansion market. This integration of multiple providers takes time and money. Overall, having to integrate multiple providers slow down business expansion and growth.

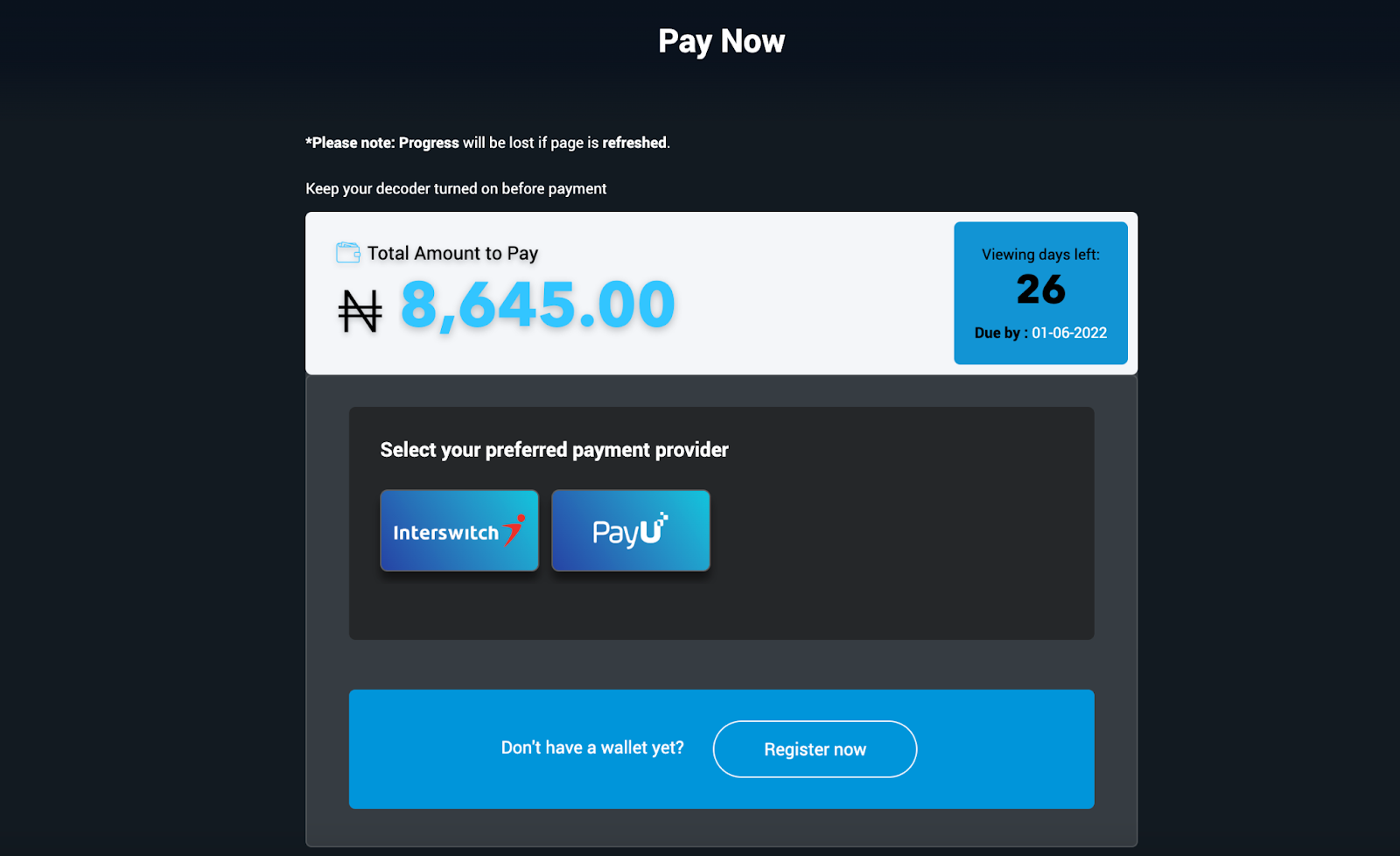

In Nigeria, Africa’s largest country, there are at least five major payment methods—debit/credit card, QR payment, USSD, direct debit, and bank transfer (spurred by virtual accounts/wallets). These methods are offered either in part or wholly by different providers like Interswitch, PayU, Paystack, Flutterwave, Stitch, and Mono. Yet, for redundancy, many merchants (like DStv) prefer to have more than one provider. The challenge with building for redundancy is that it takes a lot of effort (to standardise and unify within your system)—as each provider uses different technologies, conventions, API frameworks, and systems. So, oftentimes, integrating a “back-up” provider is just like integrating a new provider for expansion.

In the year of the Digital Bank (2018), Jerry Enebeli was a Backend Engineer at one of the newly-launched digital banks, Eyowo. As an engineer, Jerry had to integrate with multiple banks for a service that could have been served by one high-performing bank. Little wonder that his return to entrepreneurship in February 2021 (with Getwallets) was an attempt to solve a banking infrastructure-related problem.

"The general idea was to make building a wallet into any application seamless", says Jerry Enebeli, former CEO and Founder of Getwallets.

The general idea was to make building a wallet into any application seamless—Jerry Enebeli | Founder, Getwallets

A few paragraphs ago, we saw a use case for wallets—e-commerce checkout via bank transfer—but there are other use cases. For instance, with wallets, digital services like Uber can temporarily hold users’ funds and use that to seamlessly process payments for trips. This ability for users to be able to pre-fund their wallets leads to more guaranteed payments for merchants and inadvertently, an increase in revenue. Fintechs like digital banks, savings, and investment platforms also make use of wallets to power their operations.

There are three major parts to a wallet; the digital ledger (tech), underlying fund holder (regulated stores of value), and money mover (tech/regulated payment service providers). The ledger can be built by the merchant, the fund holders are limited to banks, and MMOs and the money mover is who gets the money into the wallet or out of the wallet. Wallet service providers tend to sync the required partnerships with fund holders, layer the technology and offer the whole as a single package.

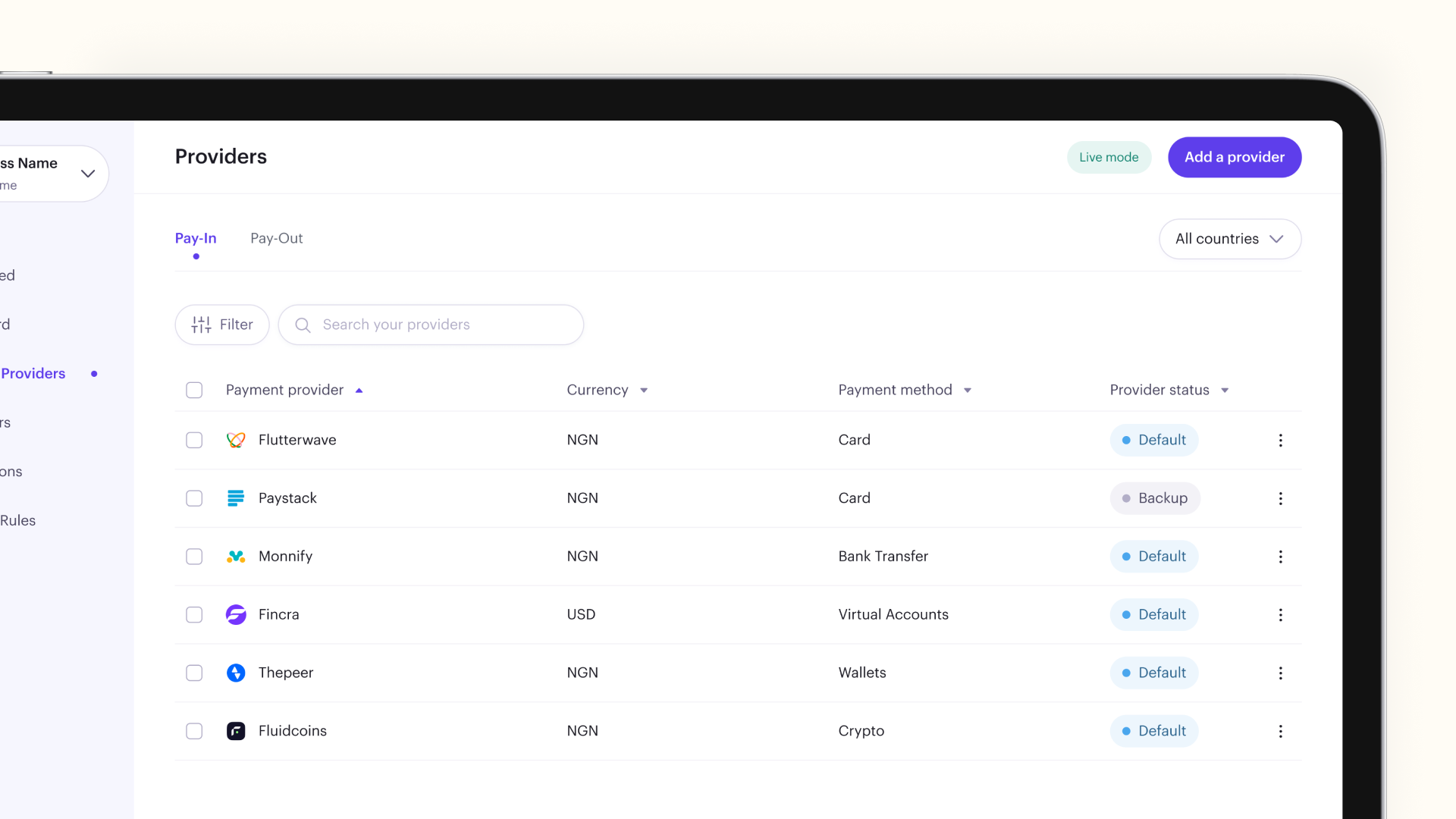

Today, in Nigeria there are many wallet service providers including Bloc, Monnify, Flutterwave, and Paystack. In SA, there is Ukheshe. While Getwallets offered wallets-as-a-Service leveraging multiple payment providers, they quickly realised that customers wanted access to the underlying provider selection technology.

“We noticed that because providers are built into our wallet we were giving people the ability to choose which provider powers money in and money out for their wallet. That single technology opened our eyes to a lot of things, people reached out saying they want that technology. This is because they've built their own ledger but they want a technology that can allow them to easily access multiple payment providers, switch from one payment provider to another if one is down.”, says Jerry Enebeli, former CEO and Founder, getWallets.

The market demand for a payment orchestration solution led the company to pivot from Getwallets to Orchestrate.

Meet Orchestrate

In December 2021, Getwallets completed the pivot to Orchestrate. With a single integration, Orchestrate provides businesses instant access to multiple payment methods and providers, globally.

This unification and simplification of payments are what the CEO and Founder of Orchestrate, Jerry Enebeli describes as their "biggest work". "Our biggest work in Orchestrate is taking the uniqueness of each payment provider and converting it to a single identity/structure."

"It's not an easy thing to do. Imagine the way Paystack looks and the way M-Pesa looks and try to give our customers a similar experience across the board. So far, we've designed frameworks that help us fit these payment providers into that single unified structure for our customers".

What Orchestrate is doing can be likened to super aggregation, which is an emerging field in Africa. Last year, an Egyptian startup raised a $3 million pre-seed to do this which gives you an insight into the mind and votes of investors. If Orchestrate gets it right, they could own the super payments API space for sub-Saharan Africa and truly ease expansion for a lot of startups.

Orchestrate doesn’t plan to stop at aggregating payment methods and providers. They are also implementing value-added services like productising discounts and enabling coupons and other add-ons out the gate.

The Product Marketing Manager of Orchestrate, Wunmi Akinfemiwa believes that a major selling point is their unified dashboard that also provides access to insights for decision making. "Instead of managing different payment methods from four to five dashboards, you can do it all on the Orchestrate dashboard. This will help the business manager access data like peak times and days, most in-demand payment methods, and more. Knowing these helps management make informed decisions across their sales lifecycle."

With the Orchestrate automated fallback system, the manual work of having to switch to a backup provider once there is a downtime on your default provider is taken care of and can be automated by Orchestrate.

The team plans to roll out the product in the third quarter of the year. Yet, since teasing the brand last week, over 35 businesses have signed up to be on their waitlist.

It’s an exciting time for fintech in Africa. As more payment providers emerge, there would be a need for an aggregator to simplify integrations, handle intelligent routing and provide visibility into each method’s performance. Could Orchestrate be that platform and aggregator?

Comments ()