Are banks leaving for Fintechs to come in?

TLDR; They collect money and distribute the money. They earn a living from net interest.

While “banking dates back to 15th century medieval Italy”, the actual act of money-lending and money-changing is as old as money. Infact, money-changing, which is the act of converting money from one country or currency to another, is regarded as the origin of modern banking in Europe.

Good-to-know: Modern central banking started with Bank of England (1694)

Over the years, Banks have grown in importance and have become vital to the survival of an economy. Their role in the management of wealth is what has led to the tight regulation imposed on them (by a country’s Central Bank). Failures of banks can lead to the failure of an economy (think: the Great Depression).

What is a Bank?

The word ‘bank’ is derived from the Italian word ‘Banca’ which means bench. After several iterations of the word, it was later used to mean ‘bank’.

A bank is a financial intermediary that accepts and stores valuable items and provides loans to credible entities. They do this within the directive of a presiding apex bank.

Fun fact: The oldest existing bank is Banca Monte dei Paschi di Siena, headquartered in Siena, Italy, operating since 1472.

To consumers, Banks perform these 2 major functions:

1. Safety and

2. Convenience

Safety: Individuals and organisations can shift the risk of losing a valuable item (usually large amounts of money) to a third-party. Threats include artificial (i.e created by humans — like armed robbery) and natural (like flood and fire outbreak).

Convenience: Banks aid movement of money locally and internationally on behalf of a consumer. That is, they act as a payment agent. For instance, employers do not need to transport salaries to each of their employees. They can place a standing order from their company bank account to that of the employees to be executed at a set date.

How do they operate? via the “3–6–3 rule”

The 3–6–3 rule describes how bankers would give 3% interest on depositors’ accounts, lend the depositors money at 6% interest and then be playing golf at 3pm😃

The 3–6–3 rule was a long-held (unofficial) view of how banks operated. The advancements in Information Technology have afforded banks an improved way of accepting deposits and lending money.

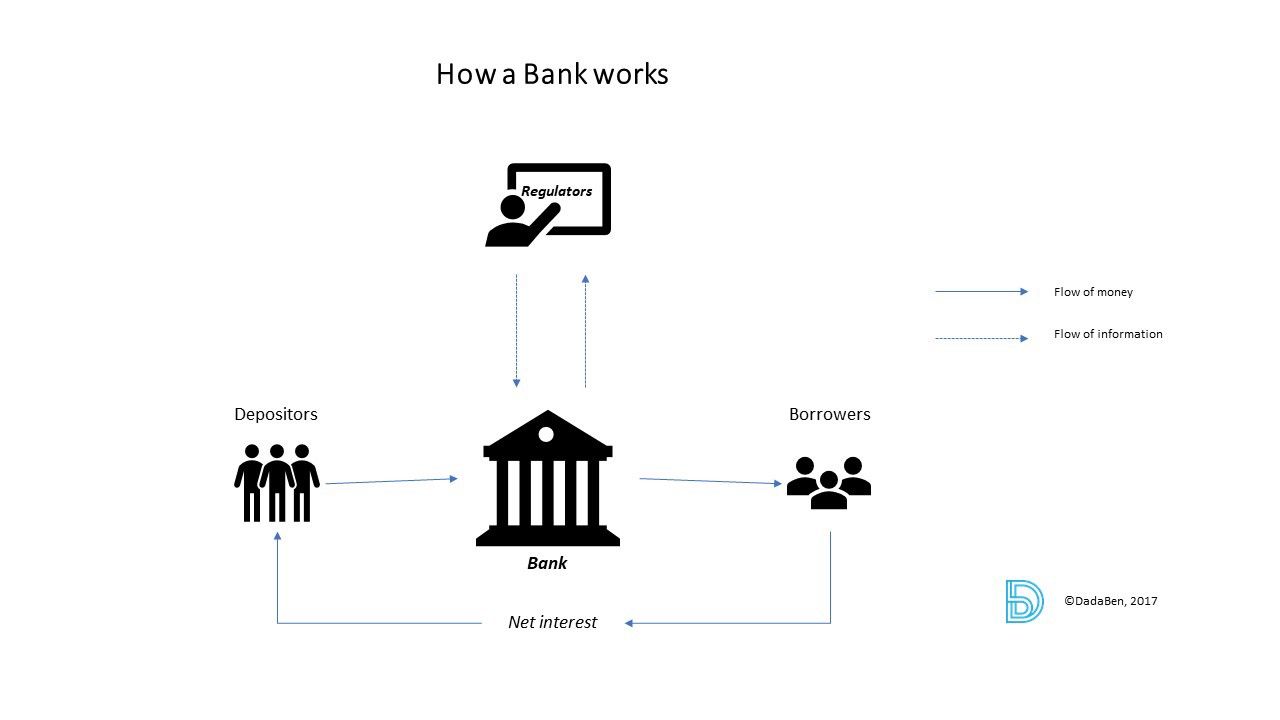

A bank’s operating model relies on its ability to make money off the spread between the high interest they receive on the loans and the meagre interest they pay to depositors (as seen in Figure 1).

The funds gotten from the net interest is then used to run the bank.

The regulators impose strict regulations on banks to mitigate the risk of another financial crisis. While the banks report back to them. In this case, there is a flow of information between both parties.

But, the other lines of communications between depositors, Banks and borrowers involves a flow of money.

It’s a cycle because when these borrowers earn a return from their investment(s), they usually plough-back profit. Thus, becoming a depositor at some bank.

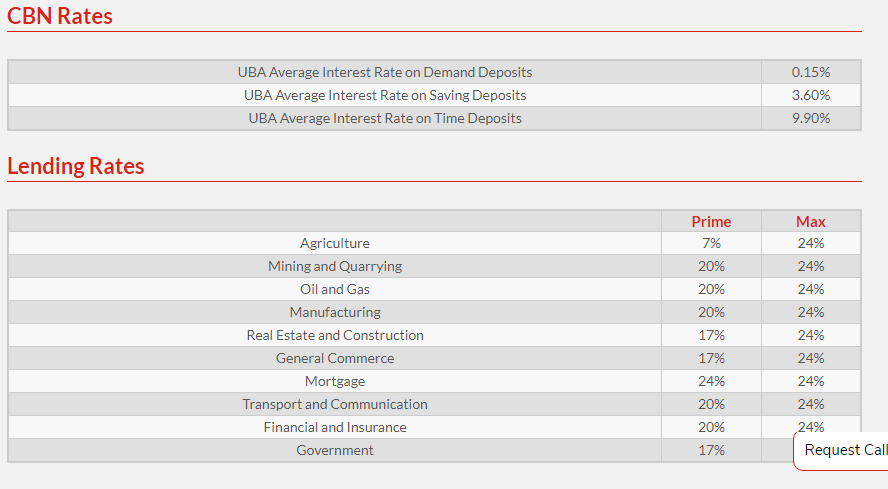

Example of net interest — UBA Savings and Lending rates

So, for instance, if Mr. Dada deposits NGN1000 into his UBA savings account he will receive an interest of 3.6% (NGN36). But, if Mrs. Ajao wants to borrow NGN1000 for a project she would have to pay back at a 17% interest rate (NGN170).

Calculating the net interest run of the bank; 170–36 = 134. We see that the bank made NGN134 on NGN1000 sitting with them. Now, imagine this same type of transaction repeated millions of times in a month. This presents one of the famous ways banks make money.

The risk involved…

The saying, “no risk, no return; high risk, high returns and vice-versa” is one financial services personnel are all too familiar with.

When a borrower needs a loan, a bank's relationship manager will work with them towards preparing a credit proposal. This then gets sent to top management depending amount and the bank's organisational structure. The idea of the credit proposal is to carry out an extensive assessment on the capacity and willingness of a borrower to pay back . This includes taking into consideration the borrower's credit history, collateral and guarantors. Thereby, lowering the chances of a repayment default.Yet, bankers still plan for possibilities of bad debt as an expense on their income statement. Because accountants are taught to recognise expenses when there is a possibility it will be incurred (see conservatism concept).

Some of the reasons for loan defaults include bankruptcy or natural disaster.

Summarily, the risk involved is in the probability of default on the repayment of the loan. Such bad debt also means that they can not earn an interest on that loan. So, now, it is beyond just losing the capital.

To protect the banked, regulatory authorities introduced fractional reserve banking. This reserve serves as a form of buffer in the event of the bank folding up (i.e becoming insolvent).

Further reading: One of such international (minimum) capital requirement regulation was defined in the Pillar 1 of the Basel Accord by the Basel Committee on Bank Supervision (BCBS).

Other ways bank make money

Asides interest runs, Banks make money in other ways. Such as direct investments in project, bank charges, spread on foreign exchange transactions, disposal of assets and claiming collateral on defunct loans ^ [Usually, if banks do not want to receive their money at a lesser value at the time of payback, they reschedule the loan. But, it is not impossible that a bank will want to impound an assets which you gave up as collateral because they can sell it at a much higher price.].

How they raise capital

Besides ploughing-back profit they also raise capital from shareholders’ equity, debt financing — like issuing bonds, inter-bank lending ^ [Inter-bank lending is a bank lending to another bank over a specified period of time. Can be one week. They are usually convenient and do not need extensive documentation.], and borrowing from the Central bank ^ [Commercial banks use the CBN’s Standard Lending Facility (SLF) window to support their liquidity shortfalls and meet trading obligations on short-term basis. Last December in Nigeria, banks borrowing from the CBN increased by 52% over the previous month. Thereby, placing the total amount borrowed at NGN2.305 trillion.]. Both the inter-bank lending and borrowing from CBN are usually short-term focused.

Heralding the Future

In the future, there will be technology disruptions and fintechs.

As early as 1994, one of the most renowned businessmen in history, Bill Gates is quoted to have said:

“Banking is necessary but banks are not”.

Fast forward two decades after, with the continued advancement of the internet and mobile, we are literally seeing banking functions being broken into fintech startups. Also, we are seeing large media and technology companies encroaching the financial services space.

Even Central banks like the Bank of England are looking to disrupt high-street banks with the introduction of Bitcoin-style currency, where customers can deposit their monies directly with them!

Naturally, these developments have caused a little panic for traditional banks which have enjoyed monopoly on deposits and some aspects of financial services. As a result, we see established banks (like Barclays) rumoured to be laying off staff worth about one-quarter of her workforce to cut cost.

Rise of FinTechs: Nigeria as a case-study

60% of Financial Services (FS) industry leaders believe a significant portion (40%) of FS business will be disrupted by standalone fintechs, according to a PwC survey report in Nigeria ‘17.

Bearing in mind that 51% of the FS business in Nigeria are run by banks. So, it won’t be too surprising to think that 40% perceived disruption will be of banks (or at least a larger part of the 40%). Whatever it is, there is a real transformation taking place.

No doubts, some fintechs in Nigeria are crushing the game and are being recognised on a global scale. Their level of execution and know-how can be attributed to globalisation and international exposure many of them have received either through leading accelerators like YCombinator or getting Venture Capital from international investors.

This is the one-time where I feel like we are actually moving at about the same pace with the rest of the world considering we had lagged behind on previous revolutions.

Here is my pick of 4 fintechs that have “modularised” banking operations and have turned it into successful startups (or in the process of doing so):

- Piggybank.ng, a two-year old fintech startup launched to help people save and by the end of 2017 their users had saved almost NGN1Billion. And they are still growing. Saving is a major function of Banks but now, new players like PiggyBankNG are encroaching into that space

- Paylater, another fintech startup offers small loans via an android app

- Paystack serves as a payment intermediary. Recently, they launched a feature called Paystack Transfer, “a feature that allows Paystack merchants to store their revenue inside Paystack as a balance, and then use that store of value to transfer money to any Nigerian bank account”.

- Bitkoin [new entrant], a fintech that offers the ability to buy and sell bitcoin in Africa.

Trivia — My pick of new-age fintechs and them reaching unicorn status

I'm here for the first Nigerian unicorn.

— 🇳🇬 benjamindada.com (@DadaBen_) January 4, 2018

My bet is on one of the FPP's all of which are FinTechs.

F - Flutterwave

P - Paystack

P - PiggyBank

The impact of fintechs will be further felt over time. But their significance to the broader Financial Services industry is such that they aid in closing the gap between the financially excluded and underserved population, so in one sense we can say they are complementing the traditional banks.

In 2016, the percentage of adults (over 18-years) in Nigeria reported to be financially excluded was put at 48%, according to a report by the EFInA. They define financial exclusion as not having or using deposit money banks, other formal or any informal financial services. If they borrow or remit they do this through family and friends; if they save, they save at home.

But the growth of these fintech companies spark a ray of hope. For instance, this year, PiggyBank users saved close to a billion naira, Paystack merchants increased by 6,300 and they processed 2.7 billion naira in December alone.

What Media and Tech Companies are doing in the financial services space

Top media/tech companies have already put in place structures to facilitate trade on their platforms which would usually involve payments. Thereby strengthening the value proposition of their network. For instance;

- Facebook: Allows movement of money via their messenger app.

- Google: Allows payment via AndroidPay

- Amazon: Testing out a payment service, AmazonPay

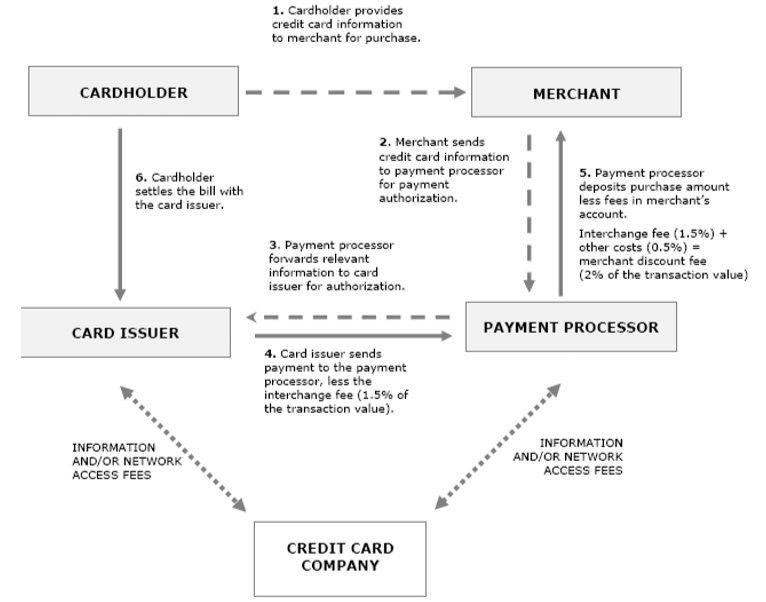

If Figure 4 is anything to go by, we see that for some big e-commerce firms like Amazon, venturing into payment processing could prove cost-reductions (in the form of interchange/transaction fee) for them. Also, it enables better and seamless integration to their core product which is the e-commerce site.

For banks, it would mean, consumers do not have to pay by bank account, as they can pay by the existing credit/monetary system on the platforms they use (sample: paystack transfers).

Next step for banks

Banks will not go extinct this year, next year or in the nearest future. Infact, it has been argued that banks are too big to fail. However, they will face a significant shift in their core consumer facing operations.

To remain relevant they can do the following things:

- Hone their other customer-centric functions like financial advising. Although, emerging technologies are making this more automated in the form of robo-advisors

- Partner with fintechs; they can serve as the back-bone for fintechs front-end operations. E.g PiggyBankNG and UBA, where UBA is the partner company that holds the fund(savings) from PiggyBankNG users.

- Invest in internal technology for innovation and growth; banks are notorious for spending big on compliance systems and we should not blame them. However, be relevant in the long-term they need to start investing in innovative technologies. They can make significant capital investments in technology because they have the funding and will create a budget once they see a need

- Continue investments in key growth sectors like Agriculture, Technology and Health

- Rebrand their offerings to institutional and individual clients leveraging already existing expertise and experience, something which these fintechs do not yet haveIn conclusion, there is work to be done. Rather than compete, collaborate, the land is green!

In summary, Banks are not leaving for fintechs to come in, together, they can drive financial inclusion at an unprecedented rate.

Originally posted on January 2, 2018.

Comments ()